HSINCHU, Taiwan — June 29, 2021 — SEMICON Taiwan, the region’s premier gathering of the entire electronics manufacturing and design supply chain, has been postponed from September 8-10 to December 2021 or January 2022 in response to a resurgence of COVID-19 cases in Taiwan, SEMI Taiwan announced today. The new event date will be announced once it has been confirmed.

The rise in new COVID-19 cases has prompted the Taiwan government to raise the pandemic alert to Level 3, forcing the closure of facilities for large gatherings such as exhibitions and conferences. SEMICON Taiwan typically draws as many as 50,000 attendees from around the world.

The rise in new COVID-19 cases has prompted the Taiwan government to raise the pandemic alert to Level 3, forcing the closure of facilities for large gatherings such as exhibitions and conferences. SEMICON Taiwan typically draws as many as 50,000 attendees from around the world.

After establishing the new event date, SEMI Taiwan will fully comply with Taiwan Centers for Disease Control guidelines for preventing the spread of COVID-19 to ensure the safety of exhibitors and visitors at SEMICON Taiwan as their well-being remains SEMI’s top priority.

About SEMI

SEMI® connects more than 2,400 member companies and 1.3 million professionals worldwide to advance the technology and business of electronics design and manufacturing. SEMI members are responsible for the innovations in materials, design, equipment, software, devices, and services that enable smarter, faster, more powerful, and more affordable electronic products. Electronic System Design Alliance (ESD Alliance), FlexTech, the Fab Owners Alliance (FOA) and the MEMS & Sensors Industry Group (MSIG) are SEMI Strategic Technology Communities, defined communities within SEMI focused on specific technologies. Visit www.semi.org to learn more, contact one of our worldwide offices, and connect with SEMI Taiwan on Facebook and LinkedIn.

Association Contacts

Elma Fang /SEMI Taiwan

Phone: 886.3.560.1777 ext. 207

Email: [email protected]

Connie Lin /SEMI Taiwan

Phone: 886.3.560.1777 ext. 211

Email: [email protected]

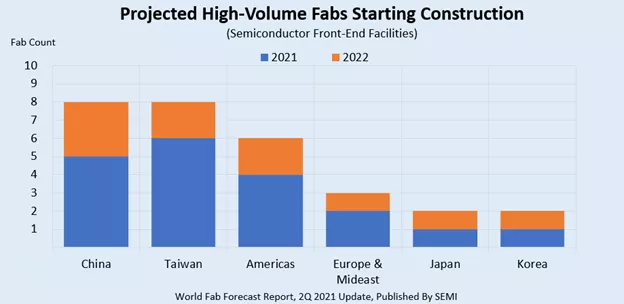

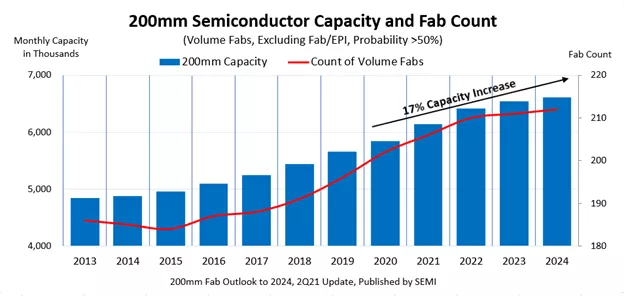

“Equipment spending for these 29 fabs is expected to surpass $140 billion over the next few years as the industry pushes to address the global chip shortage,” said Ajit Manocha, SEMI president and CEO. “In the medium and longer term, the fab capacity expansion will help meet projected strong demand for semiconductors stemming from emerging applications such as autonomous vehicles, artificial intelligence, high-performance computing, and 5G to 6G communications.”

“Equipment spending for these 29 fabs is expected to surpass $140 billion over the next few years as the industry pushes to address the global chip shortage,” said Ajit Manocha, SEMI president and CEO. “In the medium and longer term, the fab capacity expansion will help meet projected strong demand for semiconductors stemming from emerging applications such as autonomous vehicles, artificial intelligence, high-performance computing, and 5G to 6G communications.”

“May billings of North America-based semiconductor equipment manufacturers continue their trajectory of remarkable growth,” said Ajit Manocha, SEMI president and CEO. “Semiconductor equipment investments continue to register record highs as the industry takes steps to address near-term manufacturing capacity constraints.”

“May billings of North America-based semiconductor equipment manufacturers continue their trajectory of remarkable growth,” said Ajit Manocha, SEMI president and CEO. “Semiconductor equipment investments continue to register record highs as the industry takes steps to address near-term manufacturing capacity constraints.” “SEMI commends Chairman Wyden, Ranking Member Crapo, and Senators Warner, Cornyn, Stabenow and Daines for their leadership to introduce a broad investment tax credit that will strengthen U.S. semiconductor supply chains and help U.S. policies keep pace with incentive proposals around the world,” said Ajit Manocha, SEMI president and CEO. “As lead times and demand for new tools grow, ensuring that upstream tool manufacturers can claim the tax incentive is particularly important.”

“SEMI commends Chairman Wyden, Ranking Member Crapo, and Senators Warner, Cornyn, Stabenow and Daines for their leadership to introduce a broad investment tax credit that will strengthen U.S. semiconductor supply chains and help U.S. policies keep pace with incentive proposals around the world,” said Ajit Manocha, SEMI president and CEO. “As lead times and demand for new tools grow, ensuring that upstream tool manufacturers can claim the tax incentive is particularly important.” Experts from Altimeter, Dell Technologies, IBM, Bank of America, Deloitte, McKinsey & Company, Disruption Advisors, Cornami and TechSearch will explore the COVID-19 pandemic’s acceleration of digital transformation and discuss new solutions and business models for the microelectronics industry.

Experts from Altimeter, Dell Technologies, IBM, Bank of America, Deloitte, McKinsey & Company, Disruption Advisors, Cornami and TechSearch will explore the COVID-19 pandemic’s acceleration of digital transformation and discuss new solutions and business models for the microelectronics industry. “The strong investments in federal research related to semiconductors and significant, multi-year funding for the Section 9902 incentive program at the Department of Commerce will significantly improve U.S. competitiveness in this vital industry, strengthen a wide range of technology-reliant U.S. supply chains, create thousands of jobs, and keep pace with programs and proposals around the world,” said Ajit Manocha, SEMI president and CEO. “With semiconductor manufacturing facilities, or fabs, heavily reliant on a complex supply chain of equipment and materials providers, the Section 9902 program must support fab suppliers to strengthen the entire semiconductor supply chain. Talent is another critical industry need, and the bill will also make investments in education and workforce development by helping students access better quality science, technology, engineering, and math (STEM) education, while strengthening technical education and incumbent worker training programs.”

“The strong investments in federal research related to semiconductors and significant, multi-year funding for the Section 9902 incentive program at the Department of Commerce will significantly improve U.S. competitiveness in this vital industry, strengthen a wide range of technology-reliant U.S. supply chains, create thousands of jobs, and keep pace with programs and proposals around the world,” said Ajit Manocha, SEMI president and CEO. “With semiconductor manufacturing facilities, or fabs, heavily reliant on a complex supply chain of equipment and materials providers, the Section 9902 program must support fab suppliers to strengthen the entire semiconductor supply chain. Talent is another critical industry need, and the bill will also make investments in education and workforce development by helping students access better quality science, technology, engineering, and math (STEM) education, while strengthening technical education and incumbent worker training programs.” Compiled from data submitted by members of SEMI and the Semiconductor Equipment Association of Japan (SEAJ), the Worldwide SEMS Report is a summary of the monthly billings figures for the global semiconductor equipment industry.

Compiled from data submitted by members of SEMI and the Semiconductor Equipment Association of Japan (SEAJ), the Worldwide SEMS Report is a summary of the monthly billings figures for the global semiconductor equipment industry.

“April billings of North America-based semiconductor equipment marked the fifth consecutive month of record growth,” said Ajit Manocha, SEMI president and CEO. “Equipment manufacturers continue to log steady growth as the industry works to meet accelerating demand for semiconductors across a wide range of end-market segments.”

“April billings of North America-based semiconductor equipment marked the fifth consecutive month of record growth,” said Ajit Manocha, SEMI president and CEO. “Equipment manufacturers continue to log steady growth as the industry works to meet accelerating demand for semiconductors across a wide range of end-market segments.”

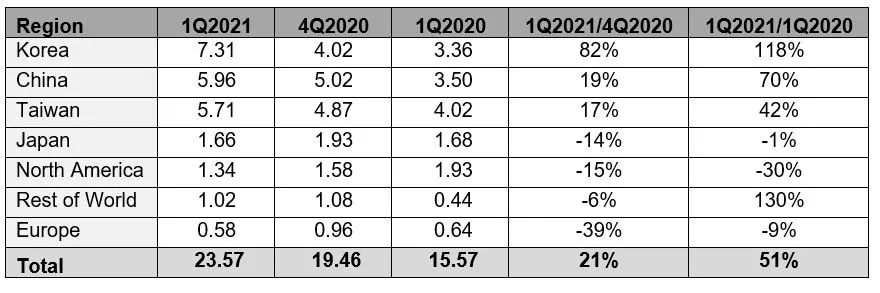

“Logic and foundry continue to drive strong demand for silicon wafers,” said Neil Weaver, chairman SEMI SMG and Vice President, Product Development and Applications Engineering at Shin Etsu Handotai America. “The memory market recovery further bolstered shipment growth in the first quarter of 2021.”

“Logic and foundry continue to drive strong demand for silicon wafers,” said Neil Weaver, chairman SEMI SMG and Vice President, Product Development and Applications Engineering at Shin Etsu Handotai America. “The memory market recovery further bolstered shipment growth in the first quarter of 2021.”