Extended Plateau, Not a New Cycle: The Broader Industry Picture

The current recovery in the semiconductor market appears to signal revival, yet is best understood as an extended phase of the existing cycle—a phase defined less by renewed demand than by structural restraint and efficiency-driven realignment.

AI-related demand is indeed driving the rebound, yet this recovery differs fundamentally from past expansionary booms. It is unfolding within an efficiency-driven adjustment phase, where capital expenditure has shifted its focus from capacity expansion to process upgrades and optimization. The observed recovery therefore reflects structural realignment rather than a conventional cyclical upswing.

This realignment has created an ‘Extended Peak Plateau’—a state not of cyclical acceleration but of structural transformation. The imbalance between resilient equipment and materials spending and stagnant wafer shipments has produced an uneven recovery, concentrated in select high-value segments rather than evenly across the value chain. The apparent plateau seen today stems less from broad-based demand expansion than from price-anchored growth, sustained by firm pricing in premium segments such as AI-related and high bandwidth memory (HBM) products.

At the same time, semiconductor manufacturers—particularly in memory—have adopted a supply-controlled operational strategy, emphasizing process optimization and product upgrades over large-scale capacity additions. Together, these three structural forces—supply/demand imbalance, price-anchored resilience, and efficiency-oriented adaptation—have defined the industry’s current phase, where revenue growth remains elevated but plateaued rather than accelerating or decelerating.

In this context, the recent rise in DRAM prices and continued hyperscaler investment hold implications beyond short-term variables: They determine whether the industry can sustain equilibrium without widening the amplitude of future cycles between overheating and contraction. If DRAM recovery remains purely supply-driven, the upturn will likely be shallow; conversely, a slowdown in hyperscaler investment could undermine the demand foundation itself.

This is why the report characterizes the current phase not as a “new cycle” but as an extended plateau. While AI-driven momentum has already taken hold, the transition toward a stable and balanced industry structure must pass through the filter of efficiency. This efficiency-based rebalancing will, in all likelihood, require a period of adjustment before a truly sustainable equilibrium — the foundation for the next phase of genuine growth — can emerge.

Desynchronization Between Investment and Wafer Demand: Evidence of a Structural Shift

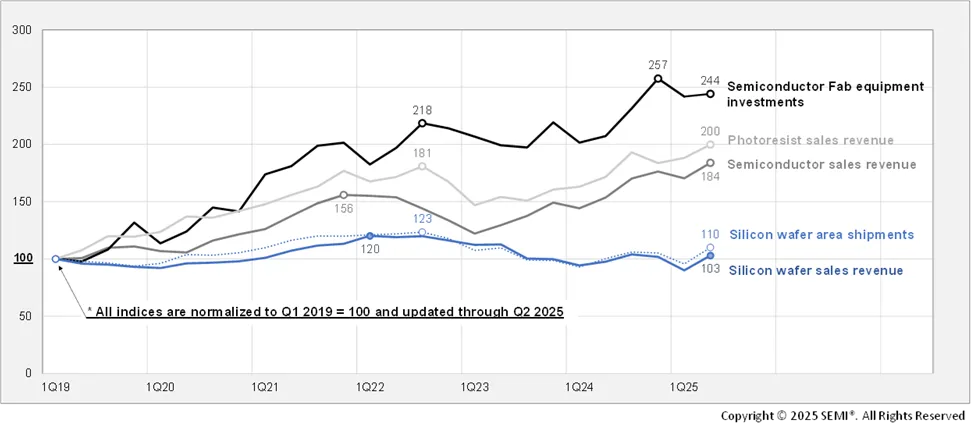

The chart below visually illustrates this structural asymmetry. When normalized to Q1 2019 = 100, as of Q2 2025 equipment investment has rebounded to roughly 244, photoresist revenue to 200, and total semiconductor revenue to 184—yet wafer shipments remain near 110 and wafer revenue around 103.

Diverging Trends Across the Semiconductor Value Chain (Q1 2019 = 100)

* Note

1. Data sources: SEMI (WWSEMS, Silicon Wafer Shipment, Photoresist Market Data), WSTS, and IR disclosures from the top five wafer suppliers.

2. Wafer revenue reflects the aggregated sales of the top five suppliers; Shin-Etsu’s quarterly figures are estimated from 2Q 2021 onward.

3. Semiconductor fab equipment investments reflect only wafer-processing equipment (WFE) expenditures, based on the Wafer Processing Equipment category defined in SEMI’s WWSEMS dataset. All indices are normalized to Q1 2019 = 100; wafer area shipments are originally reported in million square inches (MSI), while other indicators represent revenues or investments in U.S. dollars (USD).

The data clearly indicate that while equipment and materials have rebounded, wafer shipments and related revenue remain subdued. This divergence is not a matter of cyclical timing; rather, it reflects a re-alignment of the industry’s recovery dynamics, driven by process complexity and efficiency-oriented capital deployment. In other words, the widening gap between investment and wafer industry output symbolizes the industry’s transition from expansion-driven growth to efficiency-driven operations.

In previous cycles, the linear linkage of “investment expansion → production expansion” prevailed. Today, however, investment is now synonymous with process-efficiency improvement rather than capacity growth. Behind this shift lie longer cycle times, rising process complexity, and the increasing concentration of demand in AI-related nodes. More complex manufacturing now requires process sustainment, advanced process control, and continual upgrades—CapEx allocation now reflects this shift.

At the same time, a clear gap has emerged between wafer revenue and shipment growth, underscoring the divergence between financial recovery and physical output. In other words, shipment volumes have improved, but average selling prices remain subdued, signaling that the recovery is not demand-driven. This indicates that the current phase is sustained not by broad-based demand expansion, but by selective growth achieved through efficiency gains and product-mix adjustments. Despite this widening gap, the industry may give the outward impression of a steady growth plateau, since CapEx spending and high-value segments continue to post solid growth. Yet what appears as stable growth in the semiconductor and equipment market could be, in fact, a structural illusion—a state shaped by process complexity, efficiency-driven investment, and deliberate product-mix management. In short, this perceived growth is the by-product of financial and supply discipline, not the result of renewed demand momentum.

Realignment of the Wafer Industry: A Gradual 300 mm-Led Shift Anchored in Efficiency and Portfolio Strategy

As the broader semiconductor ecosystem shifts its focus from expansion to efficiency—and from scale to high value and customer reliability—wafer manufacturers are, in turn, redefining their competitive edge around operational efficiency and the stable delivery of high-value products. The 300 mm wafer segment continues to lead the recovery, whereas 200 mm wafer shipments remain significantly below its 2022 peak, constrained by sluggish demand from legacy and non-memory applications. On the profitability front, depreciation burdens and persistent pricing pressure are creating dual headwinds.

To navigate this environment, leading wafer suppliers are pursuing a dual-track approach: renegotiating long-term supply agreements (LTAs) while managing short-term contracts and selective and disciplined pricing to sustain utilization. At the same time, they are optimizing product portfolios to balance cash-flow defense with strategic offense. In this context, the critical question is shifting from “How much can be sold?” to “What kind of portfolio—specifically, how consistently can high-value wafers be sold and delivered?”

In essence, performance is now measured less by expansion and investment scale, and more by efficiency, sustainability, and reliability. This strategic realignment mirrors the broader efficiency-driven transition underway across the semiconductor value chain, underscoring that the wafer industry is no exception to the global shift toward disciplined, portfolio-centric growth.

Conclusion: The Path to True Recovery — When Three Forces Align

In summary, the current semiconductor market is best understood as having entered an extended plateau following the peak of the present cycle, with its future trajectory hinging on how effectively DRAM price resilience and Big Tech investment continuity can restore balance. In essence, the outcome will depend on the market’s ability to narrow the amplitude between overheating and contraction, moving toward a more sustainable equilibrium.

Rather than focusing on the DRAM price rebound driven primarily by supply adjustments or on demand concentrated in specific sectors, what truly matters for the wafer industry is the structural alignment of three key forces: (1) the recovery of broad-based and genuine demand, (2) the stabilization of the semiconductor supply structure, and (3) the improvement of operational efficiency across the value chain. The moment these three forces align will signal the true onset of the next upcycle — not only for the broader semiconductor market, but also for the global silicon wafer industry.

Such alignment rarely occurs quickly — it requires time, discipline, and structural patience.

This article distills the key insights from the Market Update section of the Q3 2025 Silicon Wafer Market Monitor Report.

In this quarter’s analysis, the focus lies on the semiconductor cycle’s transition into an Extended Peak Plateau — a phase characterized not by broad-based expansion, but by efficiency-driven operations and portfolio realignment. Drawing on shipment, revenue, and CapEx data across wafers, materials, and equipment, this section identifies structural asymmetries between investment and shipment dynamics, and explores how efficiency gains, product-mix optimization, and supply discipline are reshaping the industry’s recovery trajectory.

Separate from this focused article, the full SEMI Silicon Wafer Market Monitor Report provides a wider array of charts and indicators, offering a multidimensional perspective on how key variables interact to shape the future of the global wafer industry. Rather than serving as background commentary, the full report aims to deliver data-driven, decision-ready insights that support strategic thinking amid persistent market uncertainty.

For more information on the report or to subscribe, please contact the SEMI Market Intelligence Team at [email protected]. Details on SEMI market data are available at SEMI Market Data.

Sungho Yoon is a Principal Analyst on the SEMI Market Intelligence team.