Americas and APAC Region Reported Double-Digit Year-over-Year Revenue Increase

MILPITAS, Calif. — April 13, 2026 — Electronic System Design (ESD) industry revenue increased 10.3% to $5,466.3 million in the fourth quarter of 2025 from the $4,955.2 million registered in the fourth quarter of 2024, the ESD Alliance, a SEMI Technology Community, announced today in its latest Electronic Design Market Data (EDMD) report. The four-quarter moving average rose 10.1%, based on a comparison of the most recent four quarters to the prior four.

“The electronic design automation (EDA) industry continues to report strong year-over-year revenue growth in Q4 2025,” said Walden C. Rhines, Executive Sponsor of the SEMI Electronic Design Market Data report. “Product categories CAE, PCB and MCM, Semiconductor IP (SIP), and Services all reported gains. Geographic regions including Americas, EMEA, and APAC reported growth in Q4, with a double digit increase in Americas and APAC.”

“The electronic design automation (EDA) industry continues to report strong year-over-year revenue growth in Q4 2025,” said Walden C. Rhines, Executive Sponsor of the SEMI Electronic Design Market Data report. “Product categories CAE, PCB and MCM, Semiconductor IP (SIP), and Services all reported gains. Geographic regions including Americas, EMEA, and APAC reported growth in Q4, with a double digit increase in Americas and APAC.”

The companies tracked in the EDMD report employed 71,517 people globally in Q4 2025, a 13.8% increase over the Q4 2024 headcount of 62,833 but down 2.3% compared to Q3 2025.

The quarterly EDMD report contains detailed revenue information within the following category and geographic breakdowns.

Revenue by Product and Application Category – Year-Over-Year Change

- Computer-Aided Engineering (CAE) revenue increased 9.4% to $1,887.4 million. The four-quarter CAE moving average increased 10.8%.

- IC Physical Design and Verification revenue decreased 2.6% to $777.2 million. The four-quarter moving average for the category decreased 5.1%.

- Printed Circuit Board and Multi-Chip Module (PCB and MCM) revenue rose 1.8% to $484.6 million. The four-quarter moving average for PCB and MCM rose 4.5%.

- Semiconductor Intellectual Property (SIP) revenue increased 18.3% to $2,083.2 million. The four-quarter SIP moving average rose 17.4%.

- Services revenue increased 19.6% to $233.9 million. The four-quarter Services moving average rose 15.9%.

Revenue by Region – Year-Over-Year Change

- The Americas, the largest reporting region by revenue, procured $2,473.5 million of electronic system design products and services in Q4 2025, a 13.9% increase. The four-quarter moving average for the Americas rose 10.6%.

- Europe, Middle East, and Africa(EMEA) procured $683.4 million of electronic system design products and services in Q4 2025, a 9.8% increase. The four-quarter moving average for EMEA grew 9.4%.

- Japan’s procurement of electronic system design products and services decreased 18.8% to $258.5 million in Q4 2025. The four-quarter moving average for Japan decreased 7.4%.

- Asia Pacific (APAC) procured $2,050.8 million of electronic system design products and services in Q4 2025, an 11.3% increase. The four-quarter moving average for APAC grew 12.6%.

About the EDMD Report

The ESD Alliance Electronic Design Market Data (formerly the Market Statistics Service) report presents Electronic Design Automation (EDA), SIP and Services industry revenue data quarterly. Both public and private companies contribute data to the report available from SEMI. Each quarterly report is published approximately three months after quarter close. EDMD report data is segmented as follows:

- Revenue by product category (CAE, IC Physical Design and Verification, SIP, PCB and MCM Layout, and Services) including numerous detailed sub-categories

- Revenue by geographic region (Americas, EMEA, Japan and APAC)

- Total employment at participating companies

For information about SEMI market research reports, visit the SEMI Market Research Reports and Databases Catalog.

About the Electronic System Design Alliance

The Electronic System Design (ESD) Alliance, a SEMI Technology Community, is the central voice to communicate and promote the value of the semiconductor design ecosystem as a vital component of the global electronics industry. As an international association of companies providing goods and services throughout the semiconductor design ecosystem, it is a forum to address technical, marketing, economic and legislative issues affecting the entire industry. For more information about the ESD Alliance, visit http://esd-alliance.org.

Follow the ESD Alliance

About SEMI

SEMI® is the global industry association connecting over 3,000 member companies and 1.5 million professionals worldwide across the semiconductor and electronics design and manufacturing supply chain. We accelerate member collaboration on solutions to top industry challenges through Advocacy, Workforce Development, Sustainability, Supply Chain Management and other programs. Our SEMICON® expositions and events, technology communities, standards and market intelligence help advance our members’ business growth and innovations in design, devices, equipment, materials, services and software, enabling smarter, faster, more secure electronics. Visit www.semi.org, contact a regional office, and connect with SEMI on LinkedIn and X to learn more.

The information supplied by the ESD Alliance is believed to be accurate and reliable, but the ESD Alliance assumes no responsibility for any errors that may appear in this document. All trademarks and registered trademarks are the property of their respective owners.

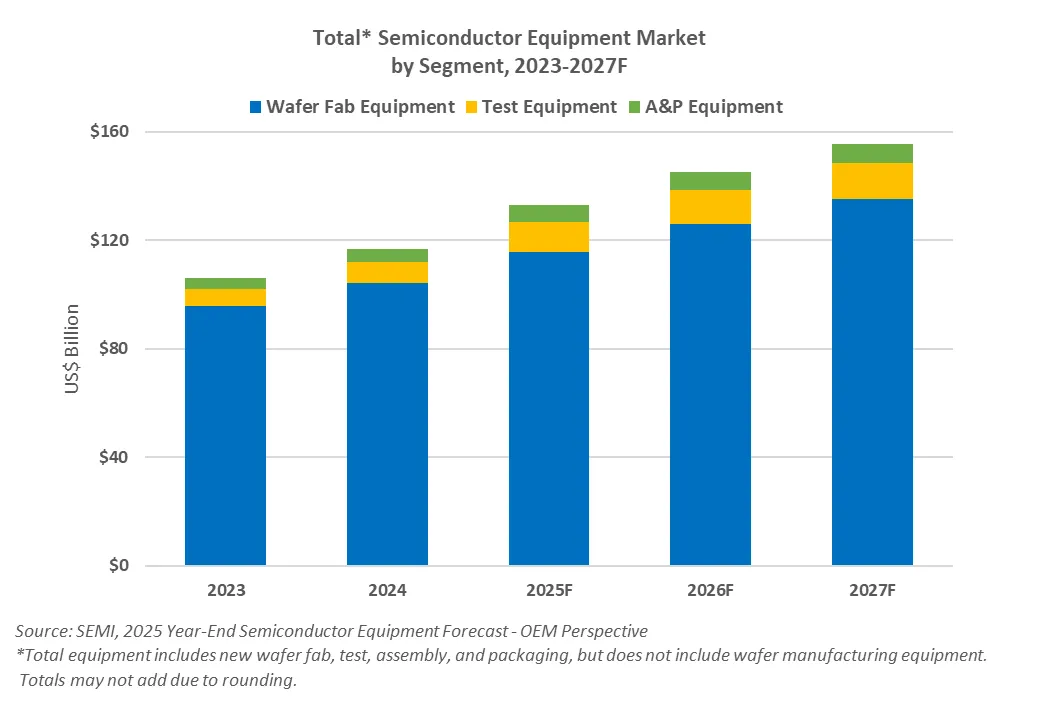

In 2025, the global front-end semiconductor equipment market posted solid growth, with wafer processing equipment sales increasing 12% and other front-end segments rising 13%. The expansion was driven primarily by continued investment in leading-edge logic and memory capacity, supported by AI-related demand and ongoing node and technology migrations.

In 2025, the global front-end semiconductor equipment market posted solid growth, with wafer processing equipment sales increasing 12% and other front-end segments rising 13%. The expansion was driven primarily by continued investment in leading-edge logic and memory capacity, supported by AI-related demand and ongoing node and technology migrations.

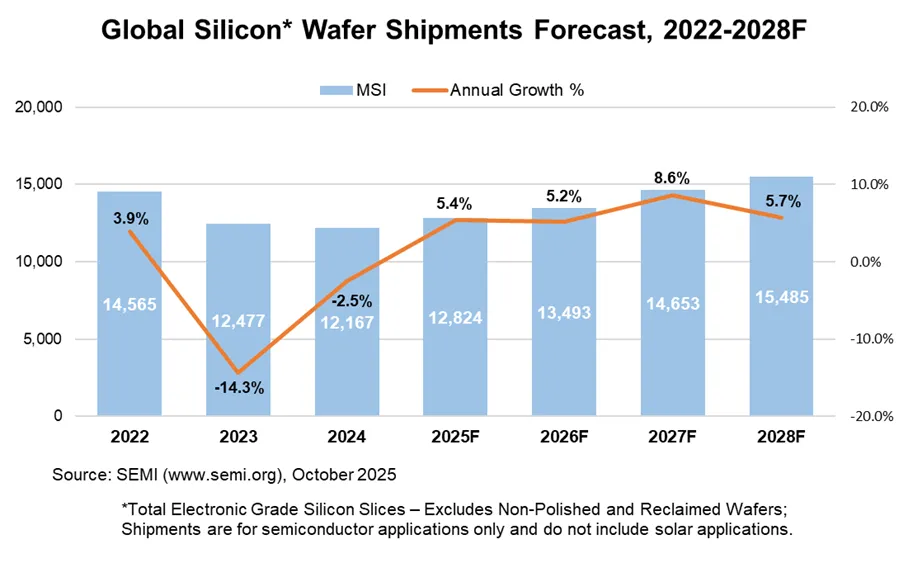

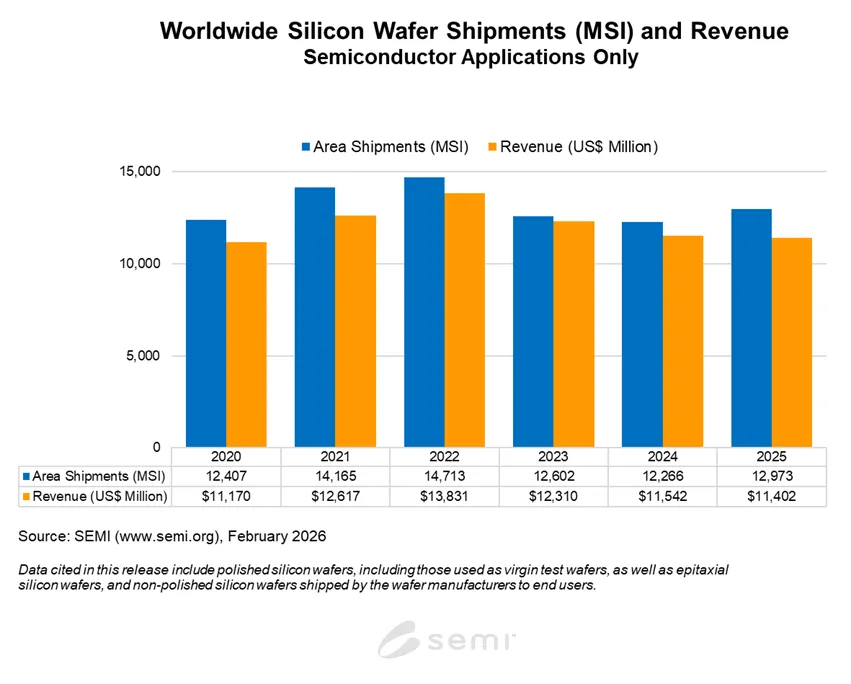

2025 marks an inflection year for wafer shipments, with silicon MSI resuming growth supported by strong demand for advanced epitaxial wafers in logic and polished wafers for high-bandwidth memory (HBM), driven by AI applications. Softness in wafer revenue is mostly attributed to the slow momentum in traditional semiconductor applications where the demand and pricing environment are yet to improve.

2025 marks an inflection year for wafer shipments, with silicon MSI resuming growth supported by strong demand for advanced epitaxial wafers in logic and polished wafers for high-bandwidth memory (HBM), driven by AI applications. Softness in wafer revenue is mostly attributed to the slow momentum in traditional semiconductor applications where the demand and pricing environment are yet to improve.

“The electronic design automation (EDA) industry continues to report strong year-over-year revenue growth in Q3 2025,” said Walden C. Rhines, Executive Sponsor of the SEMI Electronic Design Market Data report. “All product categories reported increases, with Semiconductor IP (SIP) and Services showing double digit gains. Geographic regions including Americas, EMEA, and APAC reported growth in Q3, with a double digit increase in APAC.”

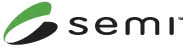

“The electronic design automation (EDA) industry continues to report strong year-over-year revenue growth in Q3 2025,” said Walden C. Rhines, Executive Sponsor of the SEMI Electronic Design Market Data report. “All product categories reported increases, with Semiconductor IP (SIP) and Services showing double digit gains. Geographic regions including Americas, EMEA, and APAC reported growth in Q3, with a double digit increase in APAC.” “Global semiconductor equipment sales show robust momentum, with both the front-end and back-end segments projected to see three consecutive years of growth, culminating in total sales surpassing $150 billion for the first time in 2027,” said Ajit Manocha, SEMI president and CEO. “Investments to support AI demand have been stronger than anticipated since our midyear forecast, leading us to boost the outlook for all segments.”

“Global semiconductor equipment sales show robust momentum, with both the front-end and back-end segments projected to see three consecutive years of growth, culminating in total sales surpassing $150 billion for the first time in 2027,” said Ajit Manocha, SEMI president and CEO. “Investments to support AI demand have been stronger than anticipated since our midyear forecast, leading us to boost the outlook for all segments.”

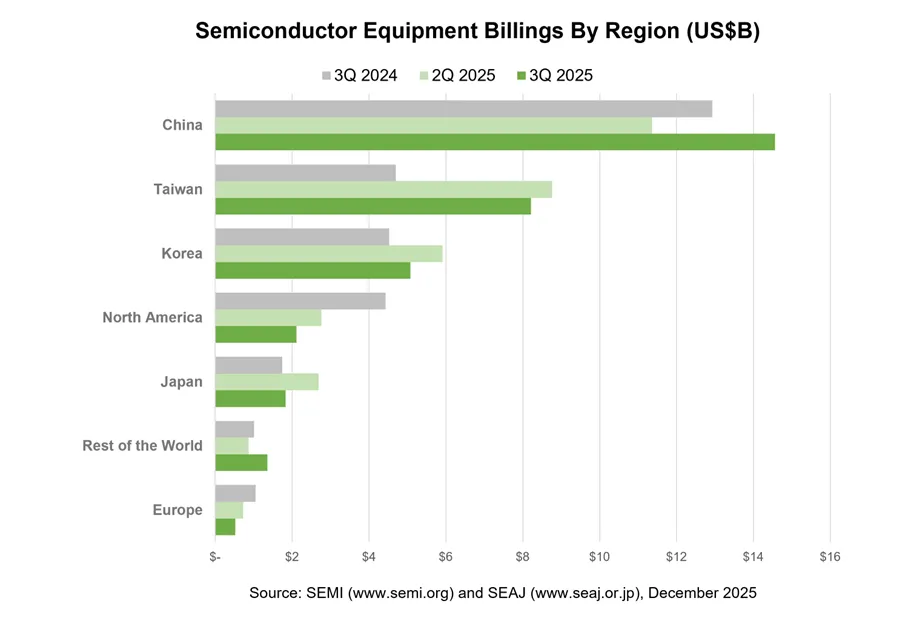

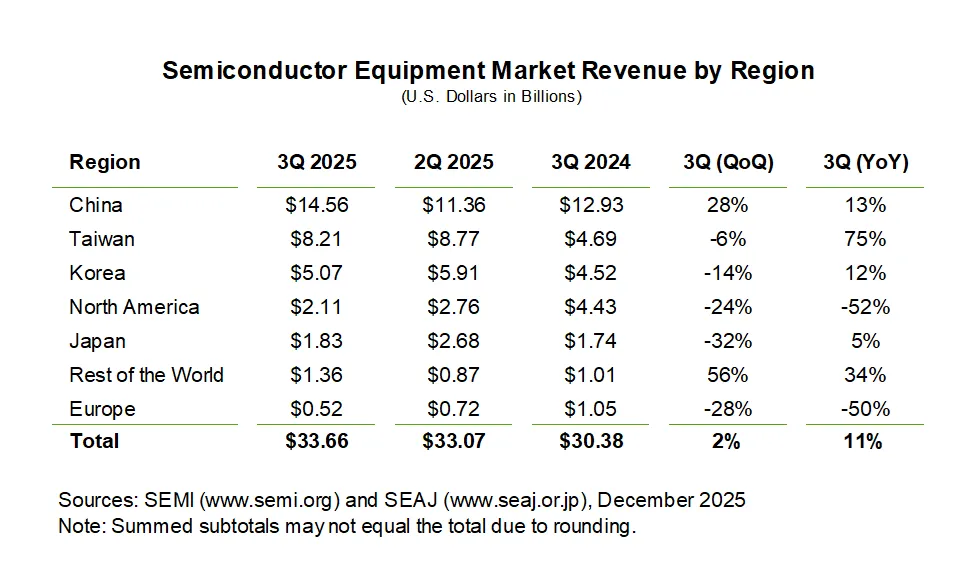

“Global semiconductor equipment billings year-to-date have reached nearly $100 billion – a record through three quarters – reflecting the industry’s sustained momentum and commitment to invest in technology innovation,” said Ajit Manocha, SEMI President and CEO. “Strong AI demand continues to drive spending in advanced logic and memory segments, as well as in packaging applications geared toward energy efficiency. This positive trajectory underscores the critical role semiconductors play in shaping a smarter and more connected world that powers next-generation digital solutions.”

“Global semiconductor equipment billings year-to-date have reached nearly $100 billion – a record through three quarters – reflecting the industry’s sustained momentum and commitment to invest in technology innovation,” said Ajit Manocha, SEMI President and CEO. “Strong AI demand continues to drive spending in advanced logic and memory segments, as well as in packaging applications geared toward energy efficiency. This positive trajectory underscores the critical role semiconductors play in shaping a smarter and more connected world that powers next-generation digital solutions.”

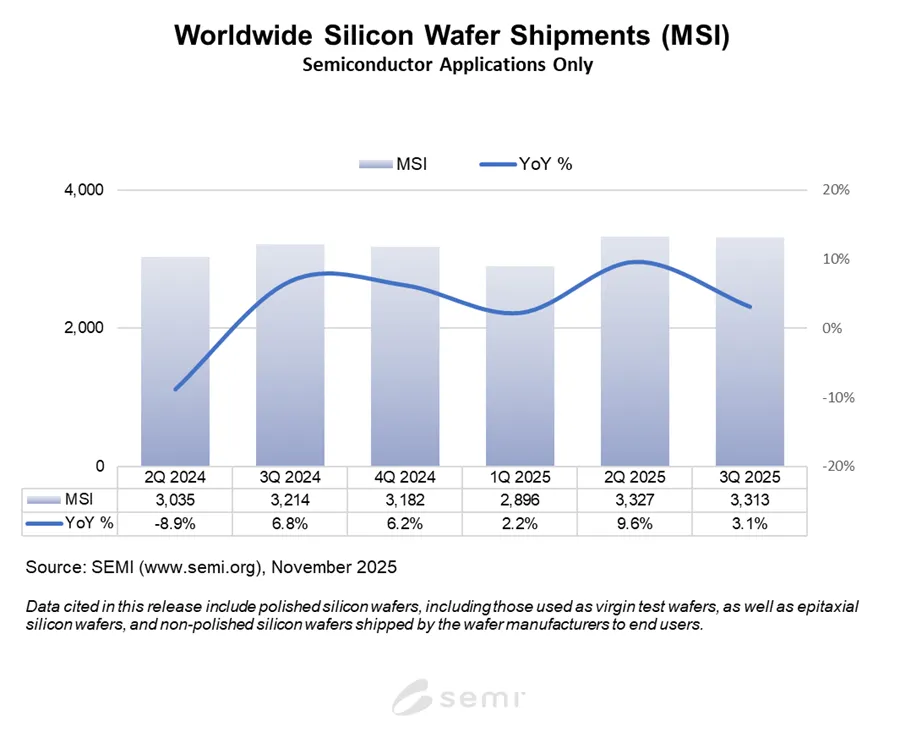

“January through September silicon shipments registered a significant year-on-year increase primarily driven by the growth of 300 mm shipments for advanced logic, cloud infrastructure, and memory demand,” said Lee Chungwei (李崇偉), Chairman of SEMI SMG and Vice President and Chief Auditor at GlobalWafers. “AI empowers significant investments expansion in advanced processes contributing to the wafer demand growth.”

“January through September silicon shipments registered a significant year-on-year increase primarily driven by the growth of 300 mm shipments for advanced logic, cloud infrastructure, and memory demand,” said Lee Chungwei (李崇偉), Chairman of SEMI SMG and Vice President and Chief Auditor at GlobalWafers. “AI empowers significant investments expansion in advanced processes contributing to the wafer demand growth.”

In 2025, the increase in silicon wafer shipments has been supported by strong AI-related growth, including advanced epitaxial wafers for leading edge logic devices and polished wafers for high bandwidth memory (HBM). Wafer shipments for non-AI applications, however, are just beginning to demonstrate a gradual recovery from the recent downcycle. The steady growth is expected to continue through 2028, driven by AI’s expanding compute footprint in data centers and at the edge.

In 2025, the increase in silicon wafer shipments has been supported by strong AI-related growth, including advanced epitaxial wafers for leading edge logic devices and polished wafers for high bandwidth memory (HBM). Wafer shipments for non-AI applications, however, are just beginning to demonstrate a gradual recovery from the recent downcycle. The steady growth is expected to continue through 2028, driven by AI’s expanding compute footprint in data centers and at the edge.