AI-fueled Investment in Leading-edge Logic, Advanced Memory, Test and Packaging Drives Five-Year Growth Surge in Semiconductor Equipment

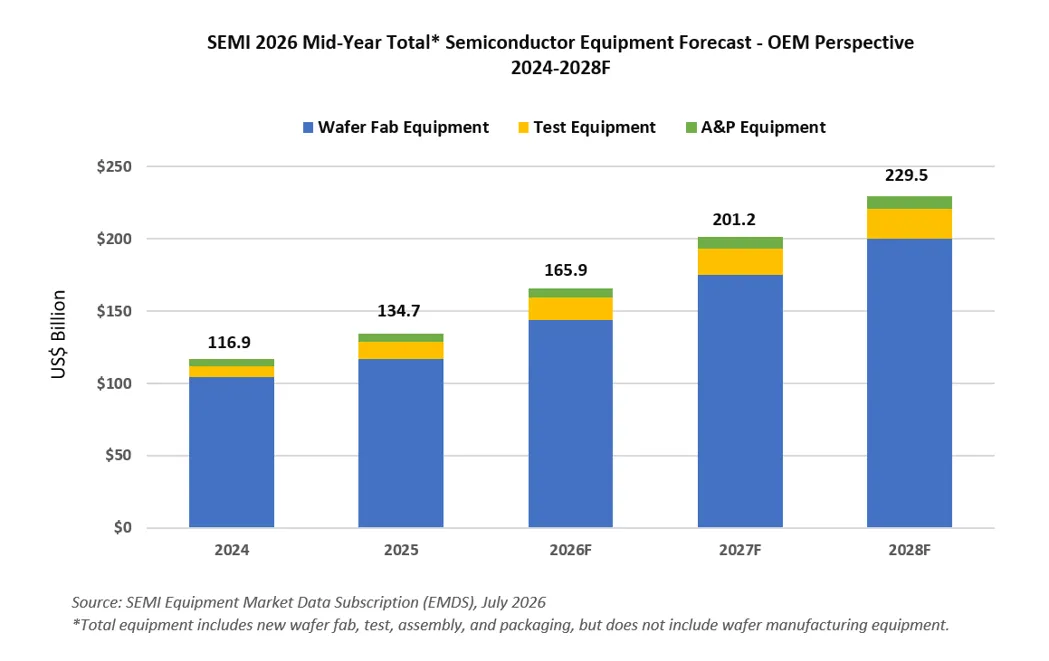

MILPITAS, Calif. — July 14, 2026 — Global sales of total semiconductor manufacturing equipment by original equipment manufacturers (OEMs) are forecast to reach a record high of $165.9 billion in 2026, increasing 23.2% year-on-year, SEMI announced today in its Mid-Year Total Semiconductor Equipment Forecast – OEM Perspective. Growth momentum is expected to continue through 2028, with total equipment sales forecast to reach a record $229.5 billion, marking five consecutive years of growth as AI-driven demand reshapes semiconductor manufacturing investment.

The stronger outlook reflects accelerating investment in AI infrastructure, leading-edge logic, advanced memory, and back-end technologies needed to support higher compute density, high bandwidth memory (HBM)-related investment, and increasingly complex device architectures.

“AI is accelerating demand for more powerful and efficient chips, driving increased investment across the semiconductor capital equipment market,” said Ajit Manocha, SEMI president and CEO. “The mid-year forecast points to a higher equipment spending trajectory as chipmakers invest in the leading-edge logic, advanced memory, test and packaging capabilities required for the AI era.”

“AI is accelerating demand for more powerful and efficient chips, driving increased investment across the semiconductor capital equipment market,” said Ajit Manocha, SEMI president and CEO. “The mid-year forecast points to a higher equipment spending trajectory as chipmakers invest in the leading-edge logic, advanced memory, test and packaging capabilities required for the AI era.”

Semiconductor Equipment Sales by Segment

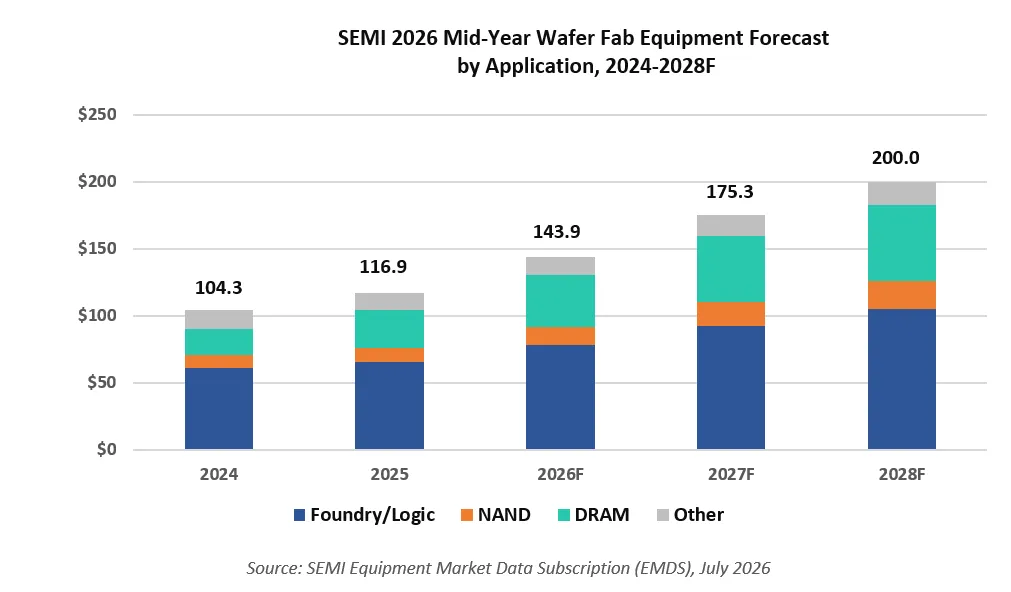

After registering a record $116.9 billion in sales last year, the Wafer Fab Equipment (WFE) segment, which includes wafer processing, mask/reticle, and fab facilities equipment, is projected to increase 23.1% to $143.9 billion in 2026. This represents a significant upward revision from SEMI’s 2025 year-end forecast and reflects stronger investment in advanced memory, especially HBM-related DRAM technologies, and leading-edge logic applications. WFE segment sales are projected to expand 21.8% in 2027 and 14.1% in 2028 to reach the $200 billion mark, as manufacturers accelerate capacity expansion and technology migration for AI-related workloads.

AI-related semiconductor demand is also driving expansion in back-end equipment. After surging 55.3% in 2025, semiconductor test equipment sales are projected to increase 31.0% to $15.3 billion in 2026, marking a strong upward revision from SEMI’s 2025 year-end forecast. Assembly and packaging equipment sales, which increased 20.8% in 2025, are projected to rise 9.6% to $6.7 billion in 2026, broadly in line with the prior forecast. Growth is expected to continue through 2028, with test equipment reaching $20.8 billion and assembly and packaging equipment reaching $8.6 billion, supported by increasing device complexity, advanced and heterogeneous packaging adoption, and more rigorous performance and reliability requirements for AI and HBM devices.

WFE Sales by Application

WFE sales for foundry and logic applications are expected to increase 18.9% year-over-year to $78.0 billion in 2026, driven by advanced-node capacity buildouts for AI accelerators, high-performance computing, and premium mobile processors. The segment is forecast to grow 18.1% in 2027 and 13.6% in 2028, reaching $104.7 billion, as the industry advances toward high-volume manufacturing at the 2nm gate-all-around node.

Memory-related equipment spending is projected to expand significantly through 2028, supported by HBM demand, advanced DRAM node migration, and NAND technology transitions. DRAM equipment sales are projected to rise 39.0% to $38.8 billion in 2026, followed by 27.4% growth in 2027 and 15.0% growth in 2028, reaching $56.9 billion. NAND equipment sales are expected to grow 30.7% to $13.9 billion in 2026, then increase 31.1% in 2027 and 14.5% in 2028, reaching $20.8 billion, driven by 3D NAND layer migration and investment in higher-density architectures.

Semiconductor Equipment Sales by Region

China, Taiwan and Korea are expected to remain the top three destinations for equipment spending through 2028. China is projected to maintain the leading position over the forecast period, though growth is expected to moderate in 2026 following elevated investment levels in recent years. In Taiwan, spending is supported by leading-edge capacity builds for AI and high-performance computing, while Korea’s equipment spending is driven by advanced memory technologies, including HBM. Other regions tracked are expected to see equipment spending increase in 2027 and 2028, supported by regionalization efforts, government incentives and targeted specialty capacity expansions.

The SEMI forecast is based on collective input from top equipment suppliers, the SEMI Worldwide Semiconductor Equipment Market Statistics (WWSEMS) data collection program, and the industry-recognized SEMI World Fab Forecast database.

About SEMI Market Data

The Equipment Market Data Subscription (EMDS) from SEMI provides comprehensive market data for the global semiconductor equipment market. A subscription includes three reports:

- Monthly SEMI North American Billings Report, an early perspective of equipment market trends

- Monthly Worldwide Semiconductor Equipment Market Statistics (WWSEMS), a detailed report of semiconductor equipment billings for seven regions and more than 22 market segments

- Bi-annual Total Semiconductor Equipment Forecast – OEM Perspective, an outlook for the semiconductor equipment market

Download a sample EMDS report.

For more information about the report or to subscribe, please contact the SEMI Market Intelligence Team at [email protected]. More details are also available on the SEMI Market Data webpage.

Follow SEMI Market Intelligence

Follow SEMI

About SEMI

SEMI® is the global industry association connecting over 4,000 companies and 1.5 million professionals worldwide across the semiconductor and electronics design and manufacturing supply chain. We accelerate member collaboration on solutions to top industry challenges through Advocacy, Workforce Development, Sustainability, Supply Chain Management and other programs. Our SEMICON® expositions and events, technology communities, standards and market intelligence help advance our members’ business growth and innovations in design, devices, equipment, materials, services and software, enabling smarter, faster, more secure electronics. Visit www.semi.org, contact a regional office, and connect with SEMI on LinkedIn and X to learn more.

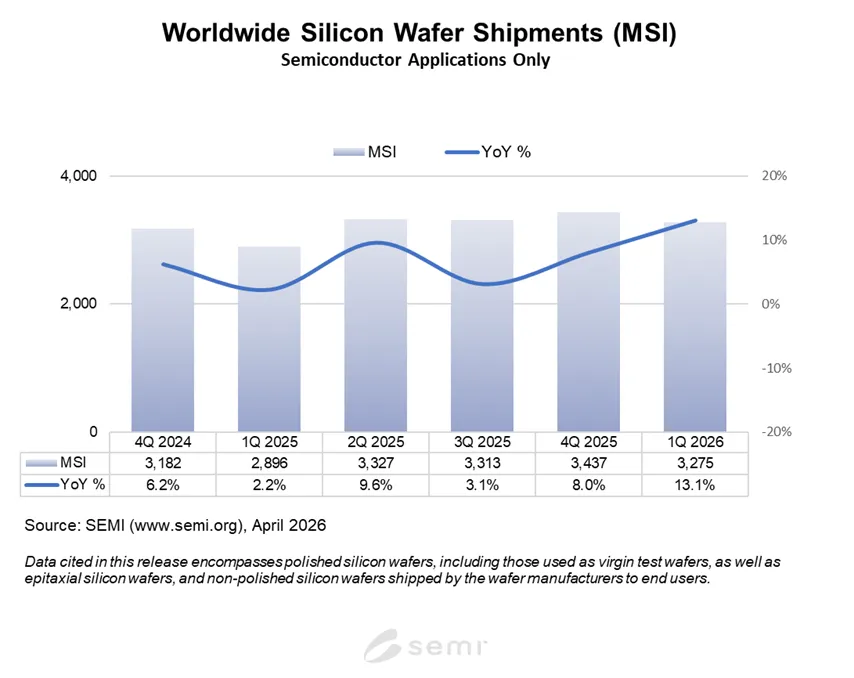

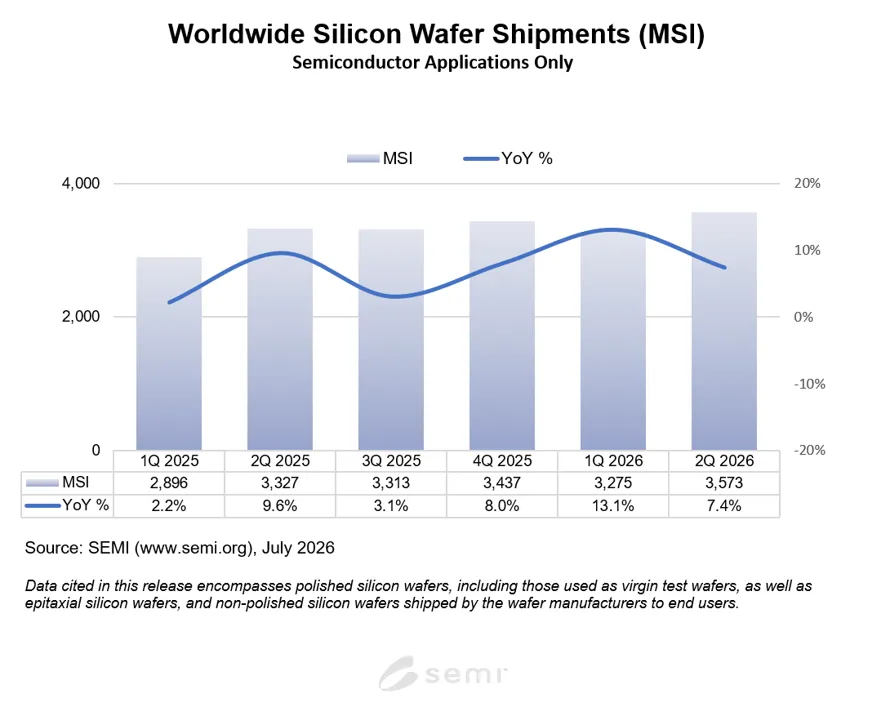

“Silicon wafer shipments maintained steady growth in the second quarter, driven by strong and increasing AI-related demand beyond advanced logic and memory to include power devices, photonics, and other markets,” said Ginji Yada, Chairman of SEMI SMG and Managing Executive Officer, General Manager, Sales and Marketing Division at SUMCO Corporation. “In addition, industrial and automotive demand is recovering, while memory price pressures are contributing to constrained PC and smartphone demand. Device manufacturers are investing heavily in capacity expansion, and silicon wafer demand growth is expected to continue.”

“Silicon wafer shipments maintained steady growth in the second quarter, driven by strong and increasing AI-related demand beyond advanced logic and memory to include power devices, photonics, and other markets,” said Ginji Yada, Chairman of SEMI SMG and Managing Executive Officer, General Manager, Sales and Marketing Division at SUMCO Corporation. “In addition, industrial and automotive demand is recovering, while memory price pressures are contributing to constrained PC and smartphone demand. Device manufacturers are investing heavily in capacity expansion, and silicon wafer demand growth is expected to continue.”

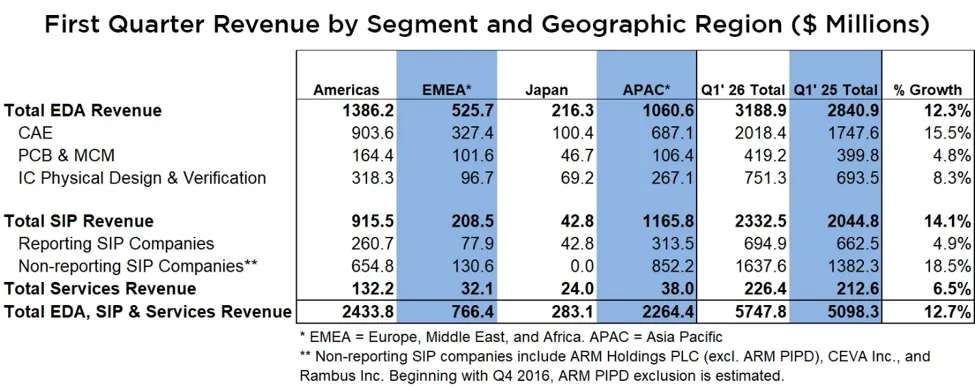

“The electronic design automation industry continued to report strong year-over-year revenue growth in Q1 2026,” said Walden C. Rhines, Executive Sponsor of the SEMI Electronic Design Market Data report and Chief Executive Officer of Silvaco Group, Inc. “All product categories reported gains, with Computer-Aided Engineering and Semiconductor IP showing double digit growth. The Americas, EMEA, and APAC geographic regions reported growth in Q1, with double digit increases in EMEA and APAC.”

“The electronic design automation industry continued to report strong year-over-year revenue growth in Q1 2026,” said Walden C. Rhines, Executive Sponsor of the SEMI Electronic Design Market Data report and Chief Executive Officer of Silvaco Group, Inc. “All product categories reported gains, with Computer-Aided Engineering and Semiconductor IP showing double digit growth. The Americas, EMEA, and APAC geographic regions reported growth in Q1, with double digit increases in EMEA and APAC.”

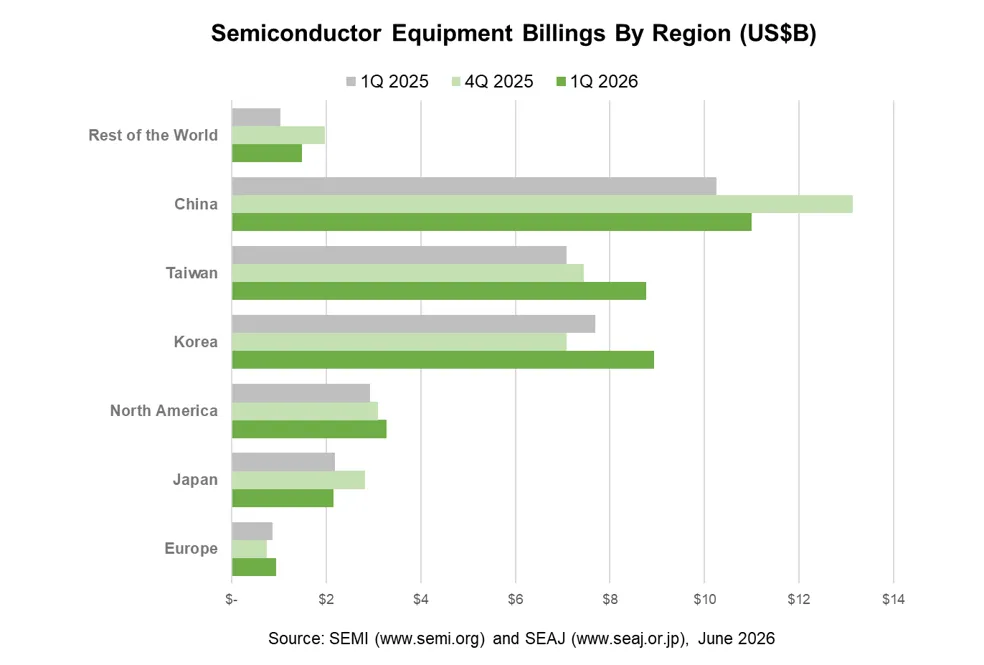

“The strong start to 2026 reflects continued industry investment in the capacity and infrastructure needed to support AI-driven semiconductor growth,” said Ajit Manocha, SEMI President and CEO. “Record first-quarter billings highlight ongoing momentum in leading-edge manufacturing and advanced packaging.”

“The strong start to 2026 reflects continued industry investment in the capacity and infrastructure needed to support AI-driven semiconductor growth,” said Ajit Manocha, SEMI President and CEO. “Record first-quarter billings highlight ongoing momentum in leading-edge manufacturing and advanced packaging.”

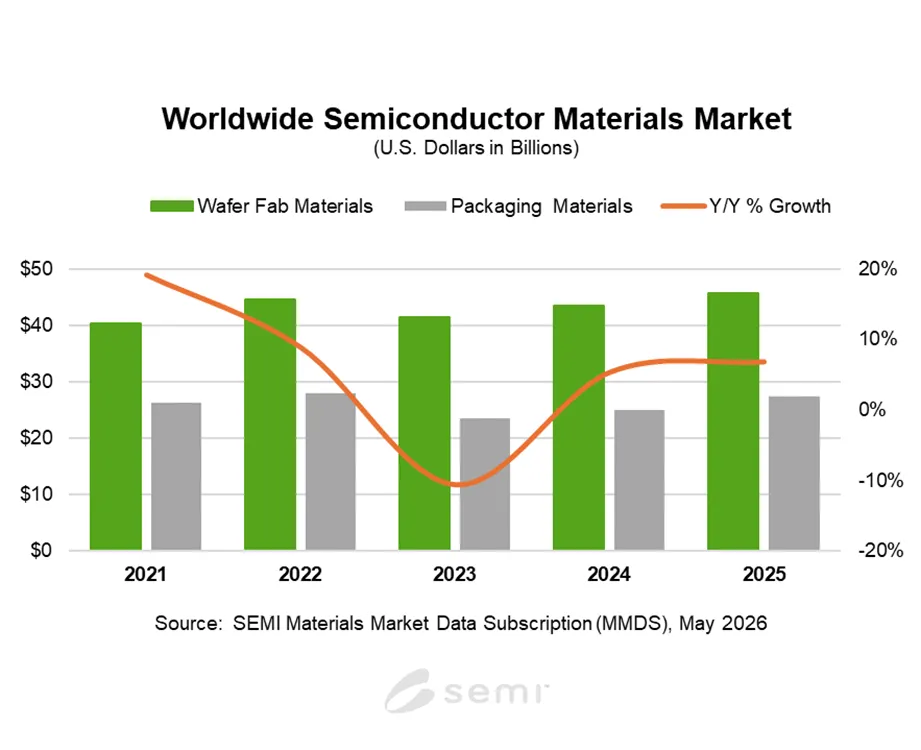

Wafer fabrication materials revenue increased 5.4% to $45.8 billion. Lithography-related materials, including photomask, photoresist and ancillaries, along with wet chemicals, posted strong double-digit growth as higher process intensity and tighter lithography requirements continued to increase materials consumption.

Wafer fabrication materials revenue increased 5.4% to $45.8 billion. Lithography-related materials, including photomask, photoresist and ancillaries, along with wet chemicals, posted strong double-digit growth as higher process intensity and tighter lithography requirements continued to increase materials consumption.