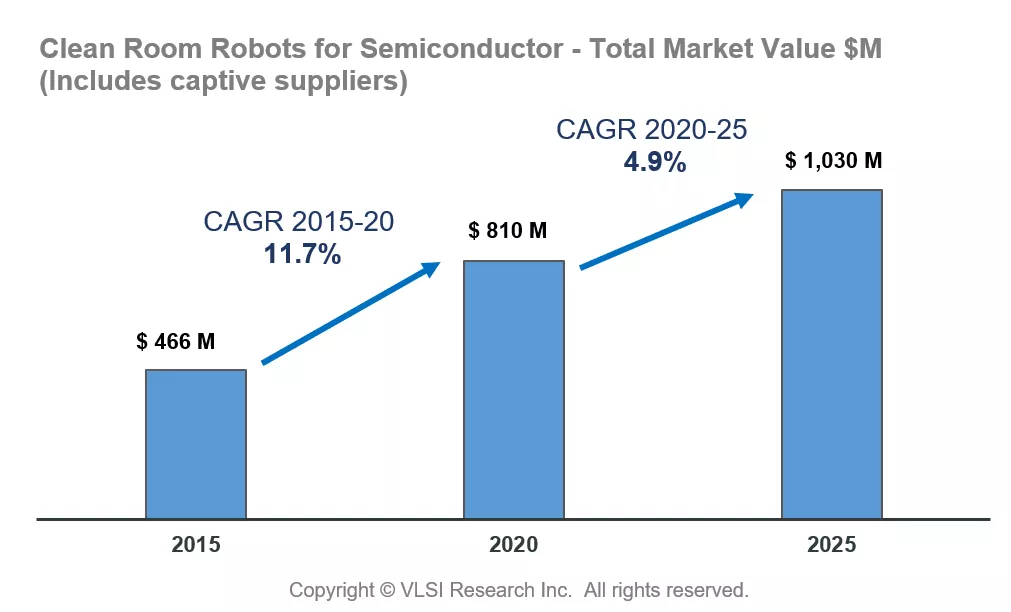

The market for vacuum and atmospheric robots used in semiconductor manufacturing equipment has grown at a compound annual growth rate of 11.7% since 2015 and is expected to top $1 billion in 2020. The historic and forecast growth trends for cleanroom robots are in line with the long-term growth rates of semiconductor manufacturing equipment.

However, breaking the data down into vacuum robots and atmospheric robots reveals a different picture. Revenues for vacuum robots grew at a CAGR of 19.9% from 2015 to 2020, while the CAGR for atmospheric robots was just 6.5%. Part of the reason for the strong growth in vacuum robots has been the increase in semiconductor manufacturing's vacuum intensity.

While additional vacuum process steps are a driver for both vacuum and atmospheric robot demand, it has the effect of increasing the share of vacuum robots as a percentage of total robots. Also, the vacuum robot market is dominated by one merchant supplier, so pricing tends to be firm. In contrast, the market for atmospheric robots is fragmented with several large suppliers, making this a very competitive environment and keeping prices for these products under pressure.

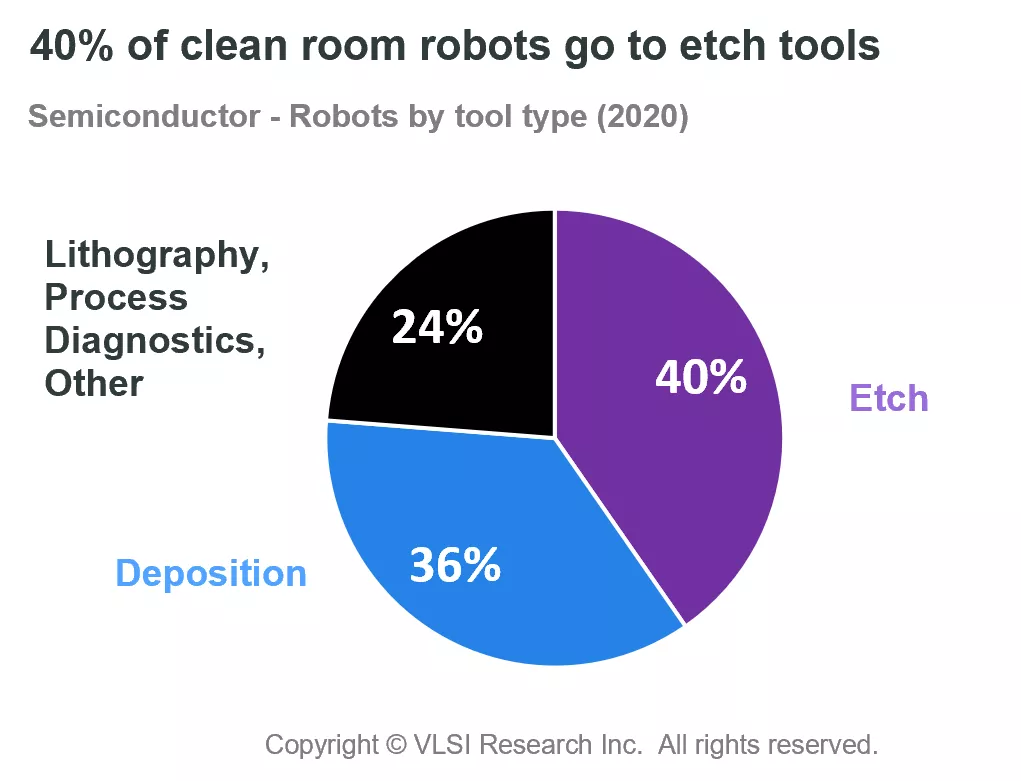

The majority of cleanroom robots are used on etch tools (40%), with 36% on deposition, and 24% on other tool types such as lithography, ion implant, CMP, process diagnostics, and wet processing.

Vendors, including captive suppliers, are mostly from North America (47%) and Japan (44%). European and Korean manufacturers supply the remaining 9% of the market.

For more information about critical subsystems, please visit VLSI Research.

John West is managing director at VLSI Research Europe.