By Dan Tracy, Industry Research & Statistics, SEMI

While 2015 started strong in terms of growth expectations, second quarter semiconductor industry information reflected a softening across various segments of the industry; PC market growth failed to materialize, tablet shipments trended flat, and lower smartphone unit growth (slowing from previously strong double-digit rates). Another dynamic impacting industry sales/revenue data was the strengthening of the U.S. dollar versus other global currencies, especially the Japanese Yen and the Euro.

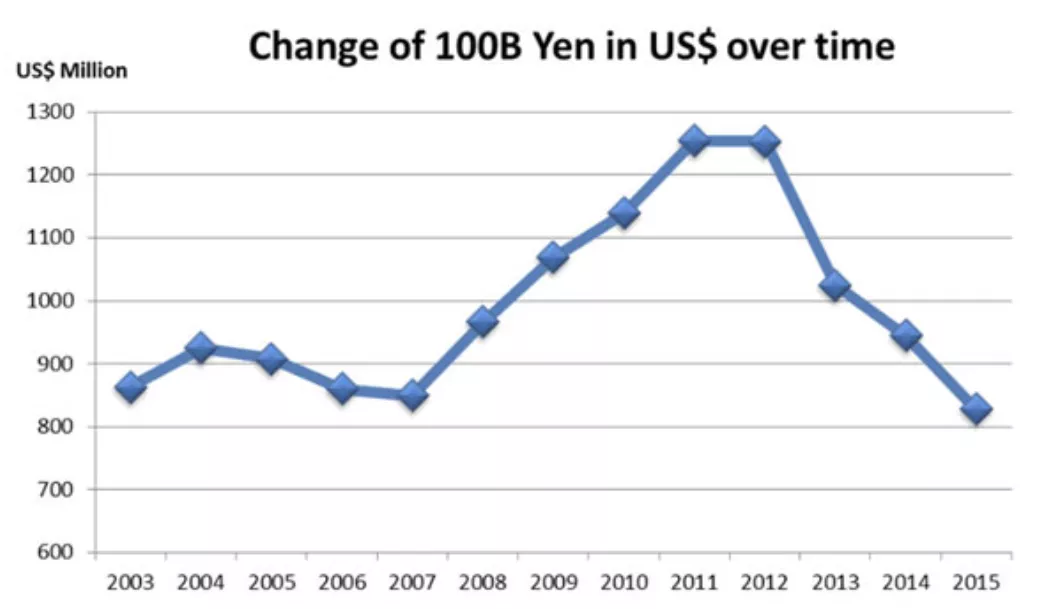

Versus the U.S. dollar, the Japanese Yen has been in decline since 2013 (see graphic), and it further weakened by another 13 percent in 2015 alone. The Euro also lost about 18 percent of its value compared to the U.S. dollar last year.

Currency trends impact semiconductor industry data expressed in U.S. dollars and this is particularly evident with the semiconductor equipment revenues as, combined, Japanese and European equipment manufacturers capture about a 55-60 percent share of the global market.

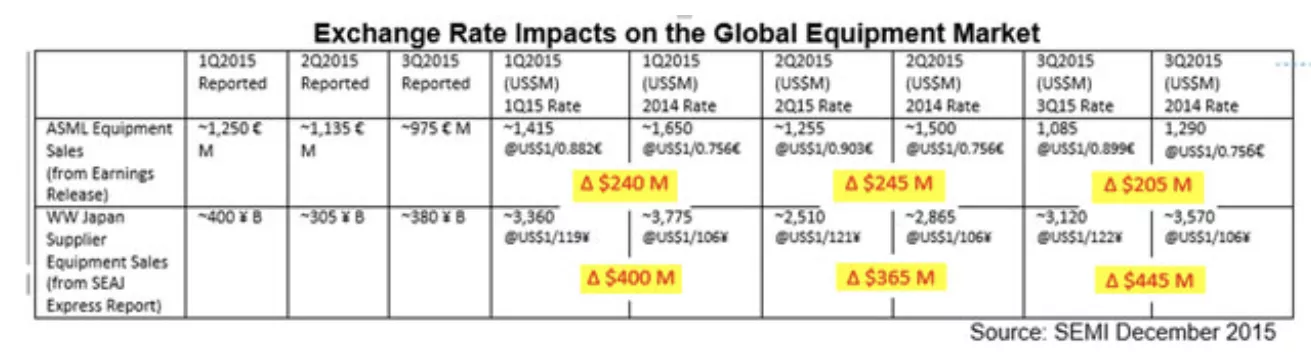

The following table summarizes the year-to-date equipment billing trends through the third quarter of the year. The 2015 equipment market through September roughly lost $2 billion or 7 percent of its value due to the Yen and Euro currency fluctuations (recalculating 2015 quarterly data assuming the average 2014 exchange rates).

In our recently issued equipment outlook for 2016, SEMI estimated that equipment revenues would decline -1% in 2015 versus 2014. Had 2015 exchange rates remained stable relative to 2014 levels (and other factors and market conditions remained the same), 2015 equipment revenues would be 5% to 6% above the $37.5 billion recorded for 2014.

One other currency change that stirred concern in some quarters during 2015 was the devaluation of the Chinese renminbi (RMB) this past August. As China’s market-driven economic growth slackened from its previously high growth rates, the national government adjusted the RMB to boost the export sector of the Chinese economy. While the change spurred some controversy, in perspective the RMB value remains in the range of the value observed in 2011/2012. (The RMB/US$ exchange rate averaged about 6.45 RMB/US$ in December).

What about exchange rate trends in 2016?

According to Duncan Meldrum, chief economist at Hilltop Economics, "With the Federal Reserve finally raising short term interest rates in the U.S., and rates elsewhere being kept the same or lowered, we can expect the dollar to appreciate even more against Asian currencies and the Euro in the beginning of the year. The resulting inward flow of capital may be enough to keep long rates from rising, however, and I expect the Fed to move slowly, so the dollar won't rise as much as it has over the past two years."

While another bout of economic—and geo-political—uncertainty has surfaced, current semiconductor industry revenues forecasts in aggregate point towards low-single digit growth for 2016. Equipment forecasts are ranging from a single-digit decline to flat to low growth (SEMI’s forecast issued in December shows 1.4 percent growth in equipment spending for the year).

For more information on SEMI Industry Research & Statistics, visit https://www.semi.org/en/products-services/market-data. Learn about China market at Window on China here: https://www.semi.org/en/resources/window-on-china

Global Update

SEMI

www.semi.org

January 12, 2016