VLSI Research recently announced the list of top suppliers of critical subsystems to the semiconductor and related manufacturing industries in 2020. The data shows that companies supplying products to chipmakers for use in the sub-fab had a good year, but those providing products directly to OEMs had an outstanding year with some vendors doubling sales.

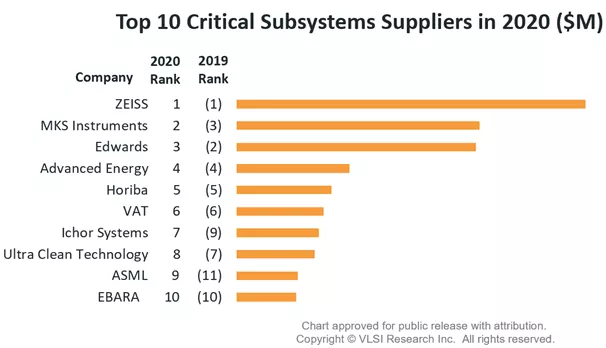

Top 10 suppliers of critical subsystems to the semiconductor, flat panel display and photovoltaic industries. Note that semiconductor sales account for approximately 86% of total critical subsystem revenues.

ZEISS retained its number one spot while MKS Instruments jumped ahead of Edwards to take second place. Edwards faced headwinds due to moderate demand for abatement subsystems and dry pumps, while MKS Instruments benefited from strong demand for RF power subsystems. Advanced Energy, the leading power subsystem supplier, widened the gap with Horiba in fifth place, and VAT held the sixth spot. Ichor Systems and Ultra Clean Technology continued to trade places, with Ichor Systems winning out this time around and taking the seventh position. ASML entered the top 10 for the first time this year as Brooks dropped out of the reckoning and just edged Ebara for ninth place.

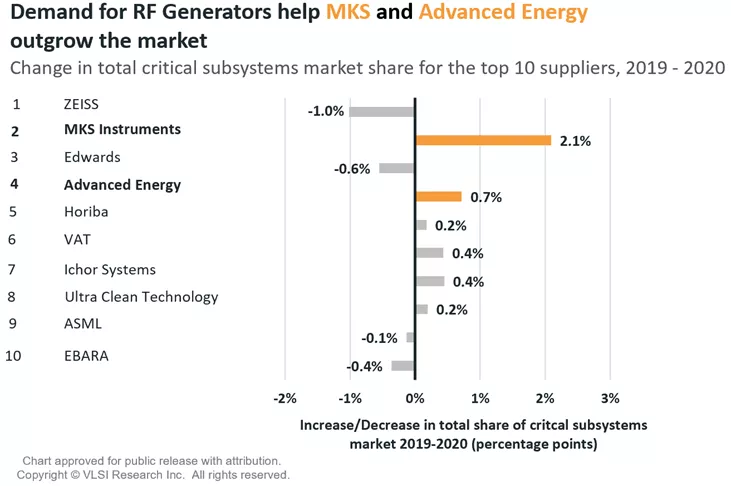

Rapid growth in shipments of dry etch chambers was a key factor in driving up demand for RF generators and matching networks. Sales of RF process power products grew 52% in 2020 compared to the industry average of 18%, and resulted in MKS Instruments, Advanced Energy, and Comet (up six places to 18th) growing their share of the overall market for critical subsystems.

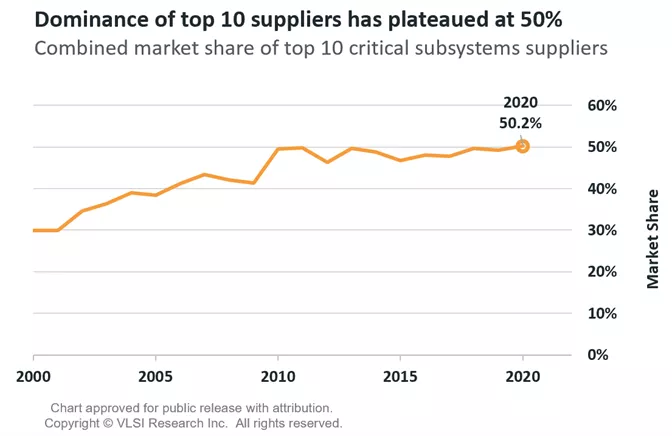

The report also highlights that the top 10 critical subsystem suppliers' dominance is reaching a plateau. Historically, the top 10 suppliers have been increasing their combined share of the market. In the 2000s, significant M&A activity (particularly in the aftermath of the financial crisis) helped consolidate the critical subsystems market. However, in the last 10 years, the combined market share of the top 10 suppliers has plateaued at approximately 50%. We believe an equilibrium level has now been reached as the leading players have strong established positions in the market and there are fewer opportunities to gain significant market share of the total critical subsystems market through mergers and acquisitions.

The source of this data came from analysis published in VLSI’s Critical Subsystems report (March 2021). For more information please visit https://www.vlsiresearch.com/public/csubs/.