報道関係各位

<ご参考資料> 米国カリフォルニア州で2019年3月12日(現地時間)に発表されたプレスリリースの翻訳です。

世界のファブ投資は2019年に減少も、2020年は過去最高へ

SEMI(本部:米国カリフォルニア州ミルピタス)は、3月12日(米国時間)、最新の2019年第1四半期版World Fab Forecastレポートに基づき、半導体前工程装置の世界市場は2019年に14%減の530億ドルとなるものの、2020年に急速に回復し27%増の670億ドルに達し、過去最高金額を更新するとの予測を発表しました。メモリー分野の減速が誘発した2019年の下降により、3年連続した装置市場の成長がストップすることとなりました。

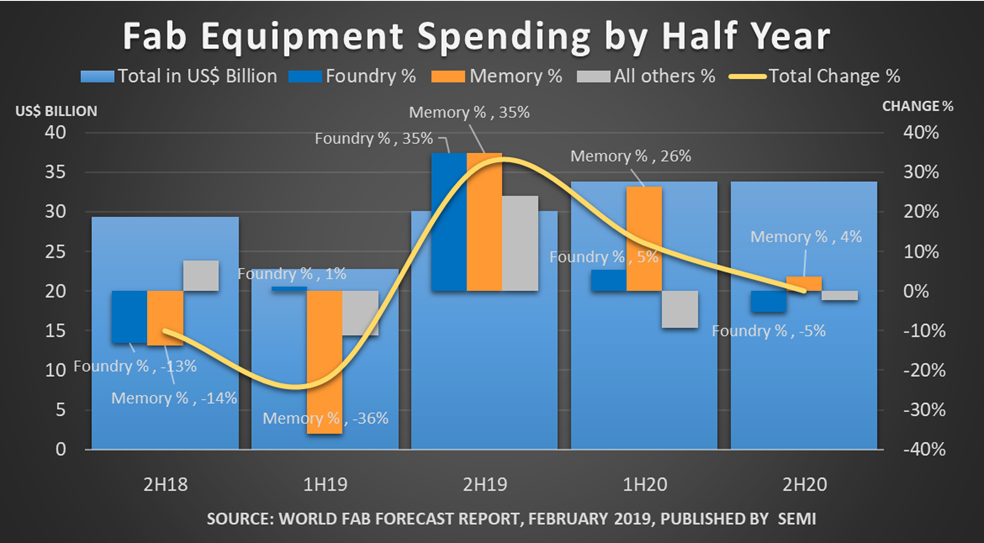

過去2年間にわたり、メモリー分野の装置投資額は、全装置市場の約55%を年間で占めていましたが、この割合が2019年に45%減少し、その後2020年に55%上昇することが予測されます。全投資額に対するメモリー分野のシェアが非常に大きいため、メモリー市場に何らかの変動が生じると、その影響が装置投資額全体に影響をします。図1は、2018年後半以降の半年毎の市場の大きな変化を、予測を含めて示したものです。

図1:ファブ装置投資額(前工程)の総額と変化率

メモリー分野の投資額減少

半年ごとのファブ装置の投資額を見ると、高水準の在庫と需要の軟化が引き起こした2018年後半のDRAMおよびNAND(3D NAND)の投資額減少が予想以上であったため、メモリー分野の装置投資額全体は14%減となりました。この減少傾向は2019年前半まで続くと予測され、メモリー分野は36%減となりますが、同年後半には35%の反発をするでしょう。

レポートによると、メモリー分野のファブ投資額は2019年後半に回復はするものの、2019年を通じては、2018年の最高記録に対して30%減となることが明らかになりました。

ファウンドリ分野の投資額も2018年後半に減少

ファブ装置の投資額で、メモリー分野に次ぐのがファウンドリ分野です。過去2年間の投資額全体に占める割合は年間25%~30%の範囲でした。2019年と2020年の年間シェアも、安定してほぼ30%を維持すると予測されます。

ファウンドリ分野のファブ装置投資額は、メモリー分野に比べて変動が小さいのが通常ですが、市場のシフトの影響をまったく受けないわけではありません。例えば、メモリー分野の投資が減少した後、ファウンドリ分野のファブ装置投資額も2018年後半に前期比13%減少しています。

SEMIのWorld Fab Forecastレポートは、1,300以上の半導体前工程ファブの投資額、生産能力、プロセスノード寸法のデータを、四半期毎、製品別に提供します。前回2018年11月版レポートから、23の新たな設備が収録されています。詳細はこちらをご覧ください。

| 本リリースに関するお問合せ | |

| 統計について: SEMIジャパン カスタマー・サービス(安藤) Email:[email protected] / Tel:03-3222-5854 | メディア・コンタクト: 井之上パブリックリレーションズ (鈴木、高野) Email:[email protected] / Tel:03-5269-2301 |